China’s Slowdown and Discounted Crude Advantage in Asia

China, the world’s largest importer of oil, is navigating a complex economic landscape in 2024. Amid the country’s economic slowdown, China’s oil demand growth has fluctuated significantly over the past few years. Despite these challenges, China and other Asian countries, particularly India, have benefited from a critical competitive edge—access to discounted crude oil from Russia. This access has allowed these nations to mitigate the impact of rising global energy prices and maintain profitability in their refinery operations. The inclusion of discounted crude has played a key role in sustaining energy supplies at more competitive costs, even as global oil prices remain elevated.

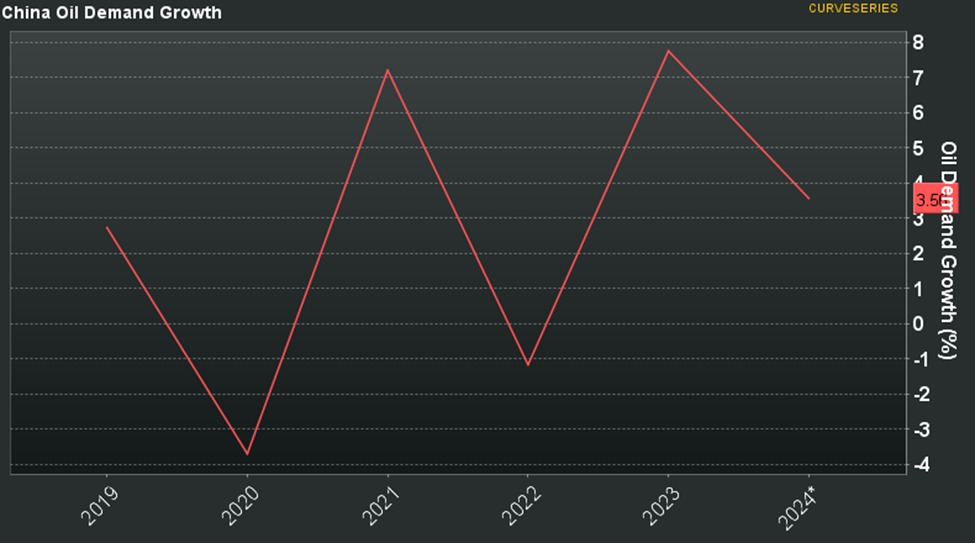

Fluctuations in China’s Oil Demand Growth

Source: OPEC

China’s oil demand growth has fluctuated significantly from 2019 to 2024, driven by both domestic challenges and global economic conditions. In 2020, demand dropped sharply by -3.7% due to the COVID-19 pandemic, which caused widespread lockdowns, reduced industrial activity, and lowered transportation needs. However, a strong recovery in 2021 saw demand surge by 7.2%, driven by government stimulus, increased industrial output, and recovering global trade.

This rebound was short-lived as oil demand contracted again in 2022 (-1.17%), due to renewed lockdowns under China’s strict zero-COVID policies, a downturn in the real estate sector, and persistent supply chain disruptions. By 2023, demand grew again to 7.75% as China lifted restrictions, leading to increased industrial production, infrastructure investment, and domestic consumption.

Looking ahead to 2024, oil demand is projected to moderate to 3.56%, reflecting the long-term impacts of an aging population, economic rebalancing, and China’s shift toward renewable energy. The transition away from fossil fuels, alongside structural economic issues like high debt levels, will likely keep oil demand growth constrained in the near future.

Leveraging Discounted Crude Oil for Competitive Advantage

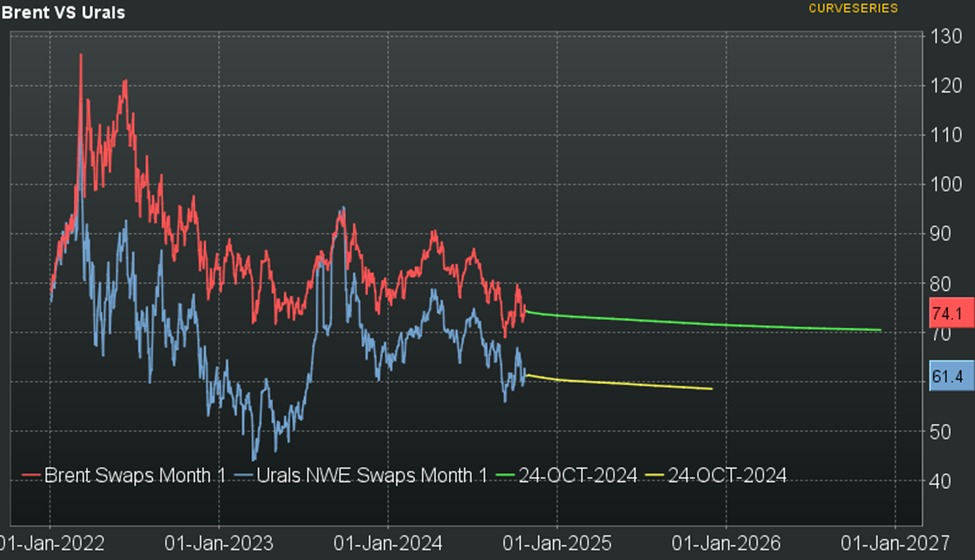

One of the critical factors supporting China’s energy sector during these periods of fluctuating demand has been its access to discounted crude oil from Russia and Iran. Ukraine in 2022 resulted in a series of sanctions imposed by the West on Russian oil exports, including a price cap of $60 per barrel DALLAS FED. This led to Russian crude, particularly the Urals grade, being sold at a significant discount to buyers in China and India.

In 2022, Brent crude oil averaged $97 per barrel, while Urals crude was priced lower at $77 per barrel, providing a $20 per barrel discount. This price differential gave China and India a significant cost advantage, as they imported Russian oil at prices well below the global benchmark. This allowed their refineries to remain profitable, even as other global refiners grappled with higher oil prices.

In 2023, Brent crude averaged $82 per barrel, with Urals crude trading at $64 per barrel, maintaining a $18 per barrel discount. This substantial price gap ensured that China and India could continue to purchase Russian crude at a discount, further enhancing their refining margins. Their ability to access cheaper oil compared to global benchmarks has been critical in keeping their refinery operations competitive and profitable during a period of global market volatility.

For 2024, Brent crude is expected to average $79 per barrel, while Urals crude is projected to trade at around $67 per barrel, indicating a smaller but still significant $12 per barrel discount. While the gap has narrowed compared to previous years, China and India continue to benefit from these discounts, which are expected to support their refining sectors as they navigate a fluctuating global oil market.

The continued availability of discounted Russian crude has allowed China and India to maintain competitive refining operations, positioning them as key players in the global energy market while Western nations face higher input costs due to sanctions on Russian oil.

Refining Margins in Asia

Refining Margins in Asia have been under significant pressure in recent years, influenced by unpredictable crude oil prices, fluctuating demand for fuel, and excess refining capacity. The sharp swings in oil prices, particularly since 2020, have created a challenging environment for Asian refineries, which rely heavily on stable input costs to maintain profitability. In 2020, the pandemic led to reduced demand for refined products like gasoline and diesel, severely impacting refinery margins. As economies reopened in 2021, margins temporarily surged due to a rapid

increase in demand, but this was not sustained.

In 2022, margins spiked dramatically, reaching nearly $35 per barrel by mid-year. This was largely driven by the rapid economic recovery following the pandemic, which boosted demand for gasoline, diesel, and other fuels. The surge in demand, coupled with supply chain disruptions, created a favourable environment for refiners, leading to a temporary period of high profitability.

However, by 2023 1H, refining margins began to decline, fluctuating between $10 and $20 per barrel during the first half of the year. The decline was driven by slowing global demand, rising inflation, and geopolitical tensions, particularly the Russia-Ukraine conflict, which disrupted global energy markets. Additionally, excess refining capacity in Asia contributed to the downward pressure on margins, as oversupply in the market made it harder for refineries to sustain high profitability levels.

In 2023 2H, margins fluctuated within a lower range of $5 to $15 per barrel. This reflects the ongoing challenges refineries face, including increasing operational costs and moderated fuel demand. The lower margins signal that profitability has been more difficult to maintain as global economic conditions remain uncertain.

By 2024, refining margins are expected to remain tight. Refineries are struggling to maintain the profitability levels seen in earlier years due to ongoing economic challenges, excess refining capacity, and subdued global demand for fuel. However, China and India have been able to maintain relatively stable refining operations by accessing discounted Russian crude oil, which has helped offset the higher global oil prices. This access to cheaper crude has been a lifeline for refineries in the region, allowing them to stay competitive despite difficult market conditions.

Sustaining Competitive Refinery Operations

Source: Trademap

In 2023, both China and India significantly increased their imports of Russian crude oil, securing cheaper supplies to sustain refinery operations and remain competitive in the global market. China’s crude oil imports from Russia grew from 8.63 million tonnes in 2022 to 10.7 million tonnes in 2023, representing a 24.1% increase. This substantial growth highlights China’s strategic reliance on discounted Russian crude oil to help stabilize its refinery sector. The availability of cheaper Russian oil has enabled China to keep refining costs lower and maintain profitability, despite higher global oil prices and ongoing economic uncertainties.

India, similarly, saw an even more dramatic rise in Russian crude oil imports. In 2022, India imported 3.68 million tonnes of Russian crude, which surged to 8.89 million tonnes in 2023, marking an astonishing 141.9% increase. This sharp rise reflects India’s increasing reliance on discounted Russian oil to reduce operational costs and improve refinery margins. The ability to import larger volumes of cheaper oil has become a crucial factor in maintaining India’s refining sector, which has faced increased global competition and rising input costs.

The combined increase in Russian crude imports for both China and India have played a pivotal role in helping these countries manage refinery margins, ensuring their refining industries remain competitive on the global stage. By taking advantage of discounted Russian crude, both nations have maintained operational resilience amid fluctuating global oil prices and economic challenges.

Conclusion

China’s economic slowdown has resulted in significant fluctuations in oil demand growth over the past few years. However, the country’s strategic access to discounted crude oil from Russia has enabled it to maintain a competitive edge in the global energy market. By leveraging cheaper oil prices, Chinese refiners have been able to mitigate the financial strain of higher global oil prices and maintain stable operations, despite challenges in domestic demand. Moving into 2024, the continued availability of discounted crude oil will remain critical to sustaining China’s energy needs and supporting its economy amid ongoing global and domestic uncertainties.